We are proud to offer Mobile Banking to all of our First Abilene FCU members. This easy to use feature offers simple menus designed for viewing on internet-enabled wireless devices making it easy to access your account 24 hours a day, 7 days a week. Here are some answers to common questions...

What can I do with Mobile Banking?

This feature allows our members to check account balances, view transaction history, transfer funds, access and use Bill Pay and view check images all from their cell phone or mobile device.

How do I use Mobile Banking?

To access Mobile Banking open the browser on your web-enabled cell phone or PDA and go to www.firstabilenefcu.org. Sign into FlexTeller using your normal username and password. From here you will be automatically be redirected to the mobile site.

Do I need a special kind of cell phone?

Mobile Banking works with most web-capable cell phones and PDAs with internet access, and supports almost all wireless service providers.

What does it cost?

FAFCU Mobile Banking is FREE to all members. Your wireless provider may charge for access or data usage based on your wireless plan.

Do I have to sign up separately for Mobile Banking?

If you are a current FlexTeller user you will automatically have access to Mobile Banking. Please update your challenge security question first if you have not done so. If you are not currently a FlexTeller user, come into either branch to fill out an enrollment form.

Can I access multiple FAFCU accounts?

Yes, as long as you have all your accounts linked together through FlexTeller you may access them all. To change between accounts go to the Setting page, select the account you want to access and click Save. Your Mobile Banking homescreen will reset to the new account you have chosen.

Can I Bookmark, add to Favorites and add to Homescreen?

Depending on your mobile devices capability you can Bookmark the mobile site, add to your Favorites and even add to Homescreen, but you must be logged in and on the mobile homescreen for these features to work.

Is FAFCU Mobile Banking safe?

Yes, FAFCU Mobile Banking is safe. Mobile Banking uses state-of-the-art security. You are protected in many ways, including: a Login ID and Password is required for access and account numbers are masked.

Tuesday, March 20, 2012

Thursday, February 2, 2012

Spending Tips: Month by Month

January:

It’s a perennial New Year’s resolution to pay down debt. So if you’re sitting on extra savings or money from the holidays, consider using it to knock off any accumulating credit card debt. Start with the credit card that has the highest interest rate.February:

Flowers can be a big part of your Valentine’s Day spending, especially if you procrastinate. If you plan on sending flower to your significant other this year, start browsing websites early to avoid excessive delivery charges on last-minute orders.

March:

If you’re planning a spring break trip always remember the best time to book a flight is four to six weeks prior to your vacation. Prices for any given flight are generally highest in last few weeks before your travel date. Another vacationing tip to remember is most airlines offer sales on Tuesday’s, Wednesday’s and Thursday’s.

April:

In honor of Earth Day use rags made from old towels, sheets or clothing when tending to common cleaning needs around the house. Also try using newspaper to help clean windows and small messes. The common family uses 2 rolls of paper towels a week costing around $120 a year.

May:

Before the weather gets too hot, have your air conditioner serviced and ready for the upcoming summer season. A clean air filter keeps your house cool and can also help your unit not run as frequently and work more efficiently, therefore saving you on your electric bill. It is suggested to change them out every 20 to 30 days in the hotter months of the year.

June:

It’s National Homeowners Month and interest rates on mortgages should still be near record lows. Prospective homeowners should start looking into the pros of buying versus renting. Homeowners should check whether it’s worth refinancing. The general rule of thumb is that the new rate should be as least 1.5 percent below your current rate.

July:

If you’re inspired by the Olympics set to take place in London, check with your local health clubs to see if they are running any discounts or special offers. This not only benefits your wallet but also your health.

August:

Several states offer tax free holidays for back-to-school items on a designated weekend. Keep up with list of needs for the upcoming school year and you could save big over this three day event. For a list of this years dates and qualifying purchases for Texas click here.

September:

Evaluate how much you spend on medication. Over-the-counter drugs are as much as 50 percent cheaper at Target and Wal-Mart than at local supermarkets, according to Consumer Reports. Also look into generic prescription offers from big box retailers, costing as little as $4 for a 30-day supply.

October:

Avoid those high price costume stores. Try to use items from around the house or borrow from friends. Local thrift stores are also a great place to find gently used costumes and props for a bargain.

November:

As our grandmothers, mothers and aunts start the hustle and bustle in the kitchen for the Thanksgiving holiday; think about buying fresh and local produce. The Farmers Market is a great place to find home grown fruits and vegetables at a great price.

December:

You don’t have to brave the crowds even if you haven’t gotten around to your holiday shopping. Sign up for to participate with retailers email list to stay on top of special sales. Hundreds of retailers also provide free shipping starting at the beginning of this busy month.

Friday, January 6, 2012

What are your 2012 Financial Goals?

It is a new year, and with that comes new goals and resolutions we all set for ourselves. Setting resolutions at the start of a new year can be effective if you create goals that are realistic and attainable. If you read any good self help book or article on goal setting the number one step is to always write it down.

When creating a good plan you want to define clear steps that can be put into action. Setting a goal without formulating a plan is merely wishful thinking. So we have come up with a form that can help you begin laying out your short, medium and long term financial goals in 2012. Click here for a printable copy.

Go ahead "Write it Down" and let us help you get started on those 2012 resolutions!

Wednesday, December 28, 2011

Tis the Season for Giving: How Giving Saves You on Your Tax Return

With so many organizations out there, it is important that your hard earned dollars are donated well and to a charity that is strong financially. You want your gift to continue to make a difference, rather than given to a charity that may or may not be here next year. Many donors do not think about these things before giving. A recent survey done by Hope Consulting found that, only about a third of donors do any research when making a charitable gift. They’re much more likely to spend time evaluating choices about jobs, business investments or vacation plans with their family.

There are no limits on charitable contributions for most taxpayers. Most taxpayers will be able to deduct cash contributions in full up to 50 percent of their adjusted gross income. For cash donations, make sure you keep all of your receipts or bank statements with proof of amount and date gift was given. For non-cash donations, make sure every time you drop off outdated clothing, household furnishings or non-perishable foods at local charities or food banks you are given a receipt. These small donation trips can add up big time come tax season. These items must be in good condition or better, according to the IRS to receive credit. Charitable gifts must be completed by Dec. 31 in order to receive these tax deductions.

Be sure to consult with your own tax advisor about your specific tax situation or refer to http://www.irs.gov/taxtopics/tc506.html for more information. If you give with your head and your heart, your giving will warm you and others for a long time to come.

Thursday, December 15, 2011

Saving Both Time & Money This Holiday Season

With the hustle and bustle of the holiday season we sometimes forget the most important reasons for the season. Use these helpful tips to help consolidate both your time and money and get back to the important things in life.

With the hustle and bustle of the holiday season we sometimes forget the most important reasons for the season. Use these helpful tips to help consolidate both your time and money and get back to the important things in life. Shop Online - Web vendors are open around the clock, 365 days a year. If you are the kind of shopper that knows exactly what you want, this is a great way to wrap up your shopping in a timely manner. Instead of spending the gas to drive across town to the mall or fighting the crowds and waiting in long lines, take 10 to 20 minutes out of your day to sit at your computer and make your purchases.

Free Shipping Day, December 16, 2011 - Started a little over four years ago, this annual event continues to grow. With over 2300 merchants involved this year, this is a great way to save on paying the higher rates to guaranteed delivery by Christmas. Most merchants participating have no minimal order and guarantee delivery by Dec. 24. Check out http://www.freeshippingday.com/ for entire list of participating merchants.

Barcode Scanning Apps for Smart Phone- Free Apps like Red Laser, Bar Code Scanner and ShopSavvy can help you compare prices by a simple scan of the UPC code. These apps make shopping a whole lot more fun. You can compare prices with local and online merchants to help you find the best deal. Most apps get as detailed as showing maps with store information and navigational tools. Don't let your successful day of shopping get ruined by finding lower prices when you get home, scan and research as you shop.

Coupon Websites - Websites such as: Groupon, Living Social, Coupon Sherpa and Yowza are not only a great way to find deals on your favorite things but also are some of the fastest growing companies in the world. These websites feature the best things to do, see, eat and buy. People love deals but hate to shop around for them, and these websites bring deals directly to you. Groupon and Living Social have daily deals on discounted gift certificates usable at local or national companies. On average they can save you between 50-60 percent. These are great tools to help you prepare for Christmas 2012! Forget getting your scissors and going through the Sunday paper, Coupon Sherpa and Yowza feature an assortment of online coupons, as well as printable, grocery and even mobile coupons. You can search by your favorite retailer's name, specific categories or by your geographical location. The sites listed above also have free mobile apps.

Group Gift Giving - Have that one gift for Mom that is just a little too much for you alone to purchase but don't want to deal with the hassle of getting the other money from your siblings? Use websites like Shareagift.com and ChipIn.com to do all the work for you. Simply set up your account with information about the gift you are wanting to purchase and amount you would like collected from each giver. An email will be sent with payable options and once funds are collected a deposit can be made into either your PayPal or bank accounts. It is that easy!

With the help from these great resources we hope your holiday buying will be easy and stress free.

Wednesday, September 14, 2011

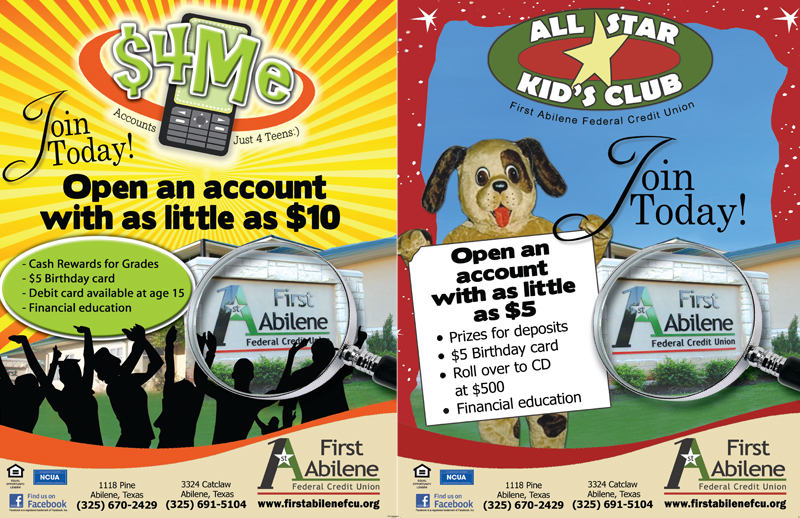

Get Kids Started Right

One good answer is a credit union share savings account. By encouraging regular savings at First Abilene FCU, you prepare your kids to meet the demands of an increasingly complex financial world. A regular savings program helps both teenagers and younger children understand the basics of personal finance and the importance of building sound money management habits. It demonstrates the power of savings to help youngsters reach their goals. It prepares them for the day when they'll manage their own money.

Even very young children can grasp the fundamentals of saving, and become excited about having their very own savings program. As they grow and acquire allowances, after-school jobs, and other income sources, children can see those savings add up--and their pride and independence grow, too.

Perhaps the most important reason to start saving early and regularly is that saving helps young people develop the skills they'll need to be intelligent credit consumers. A record of regular savings tells the credit union this young person can handle the responsibility of repaying that first loan for a car, college, or educational travel.

Having demonstrated the ability to stick to a planned program, loan officers are more likely to approve the loan application. In this situation, the share savings account does double duty, because the young borrower--lacking any credit history--can use it as security for the loan.

So don't wait. Help your children open share savings accounts and encourage them to add to them each week or month.

Remember, it's not the amount of the deposit that counts: It's establishing sound, lifelong financial habits that will make more complex financial transactions later on easier, and more comfortable.

Monday, August 1, 2011

Back to School: Plan Your Budget

Back to school means expenses! Clothes, shoes, and school supplies can drain a budget quickly. According to The National Retail Federation, the average family with school-aged children spends $606 on back-to-school items--clothes, shoes, supplies, and electronics--each year. It’s no wonder setting a budget is essential for all parents with school-bound youngsters.

To avoid falling into debt at back-to-school time, plan ahead for how much you want to spend. You also may want to budget for the changing technology of school supplies. More classrooms are using computers and computer-related study materials. And with many electronics now somewhat affordable to most families, classrooms may be requiring or recommending tech-smart supplies and materials.

Also, don’t forget about doctor checkups, school fees, and athletics or other extracurricular fees, which often are overlooked when setting a back-to-school budget.

To avoid falling into debt at back-to-school time, plan ahead for how much you want to spend. You also may want to budget for the changing technology of school supplies. More classrooms are using computers and computer-related study materials. And with many electronics now somewhat affordable to most families, classrooms may be requiring or recommending tech-smart supplies and materials.

Also, don’t forget about doctor checkups, school fees, and athletics or other extracurricular fees, which often are overlooked when setting a back-to-school budget.

Subscribe to:

Posts (Atom)